Director’s liability: Cap possible?

The new Belgian Code of Companies and Associations (BCCA) entered into force on 1 May 2019. An important reform is the introduction of the liability limitation. Are you fully protected as a director? A brief explanation.

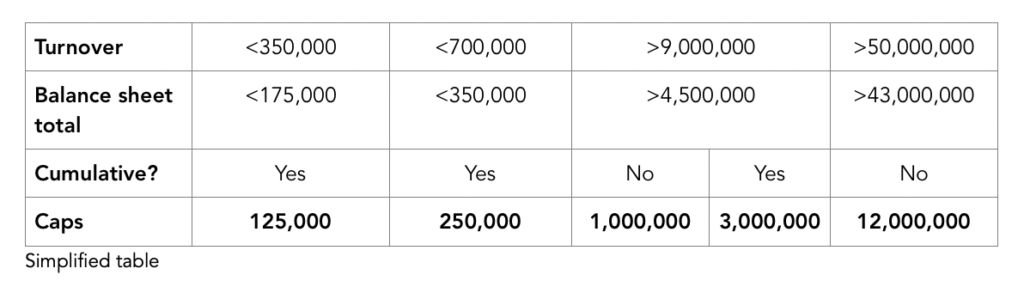

By introducing Article 2:57 of the new BCCA, the legislator introduced a limitation of liability for directors (incl. managing directors and de facto directors), the size of which is determined in function of the average balance sheet total and the average turnover of the company for the past 3 years. The caps are as follows:

The amounts apply to all directors together per act or totality of acts that can give rise to a liability claim.

These caps apply to a normal management error, a breach of the BCCA or a breach of a provision of the articles of association, as well as in the context of a failure related to a manifest gross error that contributed to bankruptcy or in the case of wrongful trading.

However, the legislator has provided for many exceptions, in particular: in the case of a minor error that occurs habitually rather than accidentally, a serious error, fraudulent intent or intent to harm, which means that the rule de facto only applies to an accidental minor error. The cap also does not apply to, among others, liability for non-payment of professional withholding tax, social security debts and incomplete paying-up of shares.

The high number of exceptions largely erodes the principle. However, in practice it appears that the introduction of the caps has made traditional D&O insurance more affordable. It remains the case that you should always exercise your mandate as director as diligently as possible.

Early repayment of professional loans: What are your risks?

You wish to repay your loan early but you see in your credit agreement a prohibition on early repayment, or the application of a (sky-high) funding loss reimbursement. What is your position?

If you qualify as an SME, and the loan was taken out after 10 January 2014 for a maximum of 1 million euros, you can invoke the Belgian SME Financing Act. In this case, your loan is repayable in advance at any time and your bank may charge a maximum early repayment penalty of 6 months’ interest. For SME loans concluded after 8 January 2018, the maximum amount was raised to 2 million euros. Important: for the purposes of the Belgian SME Financing Act, no distinction is made between a loan at interest and other forms of credit. After all, the Belgian SME Financing Act refers to civil law (Art. 1907bis Belgian Civil Code) concerning loans at interest (see below).

If you fall outside the scope of the Belgian SME Financing Act, civil law may provide a solution. The qualification of your credit agreement is important here. In the case of a “loan at interest”, the early repayment penalty is legally limited to 6 months’ interest (Art. 1907bis Belgian Civil Code), while this is not the case for other forms of credit (e.g. a straight loan). Be aware that case law usually qualifies an investment credit that is repaid at fixed times as a loan at interest. The limitation under civil law therefore applies regardless of the qualification applied by your bank.

Note that civil law does not exclude a ban on early repayment. Despite a contractual prohibition, your bank will still allow early repayment in exchange for payment of high funding loss compensation. Also note here that the aforementioned limitation of 6 months’ interest applies when it concerns a loan at interest. This was also confirmed by the Belgian Court of Cassation.

Conclusion: if you are negotiating a credit facility as a non-SME, or as an SME for an amount above 2 million euros, you have no legal protection. In this case be on your guard during contract negotiations and check the general terms and conditions.

Sara Burm and Bart Brunet

De Langhe Attorneys

Published in Voka – Ondernemers Oost-Vlaanderen editie 02/12/19