Clarification on estate planning with life insurance contracts and partnerships

In the context of estate planning, accumulated assets can be contributed to a partnership and then reinvested in a life insurance contract. The threat of inheritance tax when the life insurance contract is paid out, casted a shadow over this practice for a while. A recent decision removes these concerns, once more clearing the air for this strategy.

Use of a partnership combined with a life insurance contract

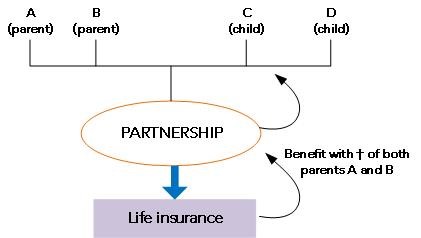

A partnership is a valuable tool in estate planning. It offers the possibility of bringing accumulated assets in the face of passing them on to the next generation while not having to immediately relinquish control of them. Furthermore, these assets can be managed and (re)invested, e.g. through life insurance contracts where this serves as a single premium. In a common situation, two parents, A and B, jointly set up a partnership to which they contribute (part of) their assets (e.g. a securities portfolio). In exchange, they receive shares which they donate to their children, C and D. The parents themselves retain either full ownership or usufruct (or a combination of both) of part of the shares.

A life insurance contract is then concluded where the actors are known to the insurance company as follows:

- Insurance contract-holder = the partnership, represented by its director(s), which is mentioned as such in all insurance documents. However, due to the lack of legal personality, the partners (A-B-C-D) are the insurance contract-holders in proportion to their shareholdership. The one-off initial premium, that has been paid consists of (part of) the assets of the partnership;

- Insured person = the last to die of A or B; and

- Beneficiary = the partnership. On the date of death of the surviving parent, the benefit will be transferred to the partnership. However, due to the lack of legal personality, the partners who are alive at that time are the insurance contract-holders in proportion to their shareholdership (most likely C and D).

It was assumed that such a structure was nothing more than a clause to benefit oneself, which does not trigger inheritance tax. Indeed, both insurance contract-holders and beneficiaries were identified as the partnership.

Inheritance tax on life insurance contracts?

In the Flemish Region, there are a number of fiction provisions that make some actions, on which in principle no inheritance tax is due, subject to inheritance tax nevertheless. One of these provisions relates to stipulations for the benefit of a third party, such as a life insurance contract. Specifically for this type of contract, this means that when someone enters into such a contract, the payment to a third party upon death, qualifies as a bequest on which inheritance tax is due.

The Flemish Tax Administration decided on the 8th of May 2023 that the aforementioned fiction provision can also apply when a partnership enters into a life insurance contract, as the beneficiary, upon the death of the insured person.

For a while, this raised concerns that all situations where a partnership contracted a life insurance contract, would be considered as a taxable clause for the benefit of a third party.

The Flemish Tax Administration nuances…

The Flemish Tax Administration recently nuanced this earlier decision, which helped to dispel the concerns. It clarified that the benefit regarding the fiction provision only refers to the portion of the benefit corresponding to the value of the shares the parents held in full ownership through the partnership.

Shares held in usufruct by the parents (or the corresponding partnership assets) thus escape inheritance tax at the time of distribution to the partnership.

Conclusion

This decision thus creates clarity – correctly, in our view – with respect to estate planning when a partnership is combined with a life insurance contract where the shares are held in usufruct by the parents. Reinvesting the assets of a partnership in a life insurance contract thus remains attractive in certain circumstances. Customised and tax-friendly planning is, as always, recommended!

Frank De Langhe – Evert Moonen

De Langhe Attorneys